This morning (03/07/2016) was our second official day at Santiago, Chile. Only a day after a warm reception at the Solace Hotel and an awesome city Tour, we kicked off our official class content with three meetings with two local entrepreneurs /and a senior manager from Microsoft Chile. The first two meetings were at the cute restaurant El Castillo in downtown Santiago, for the third and last meeting of the day we went to Microsoft headquarter. For this post, I will focus on the meeting with Guillermo Acuña, General Manager of Cumplo (“La rede de financiamento transparente” or financial transparent network).

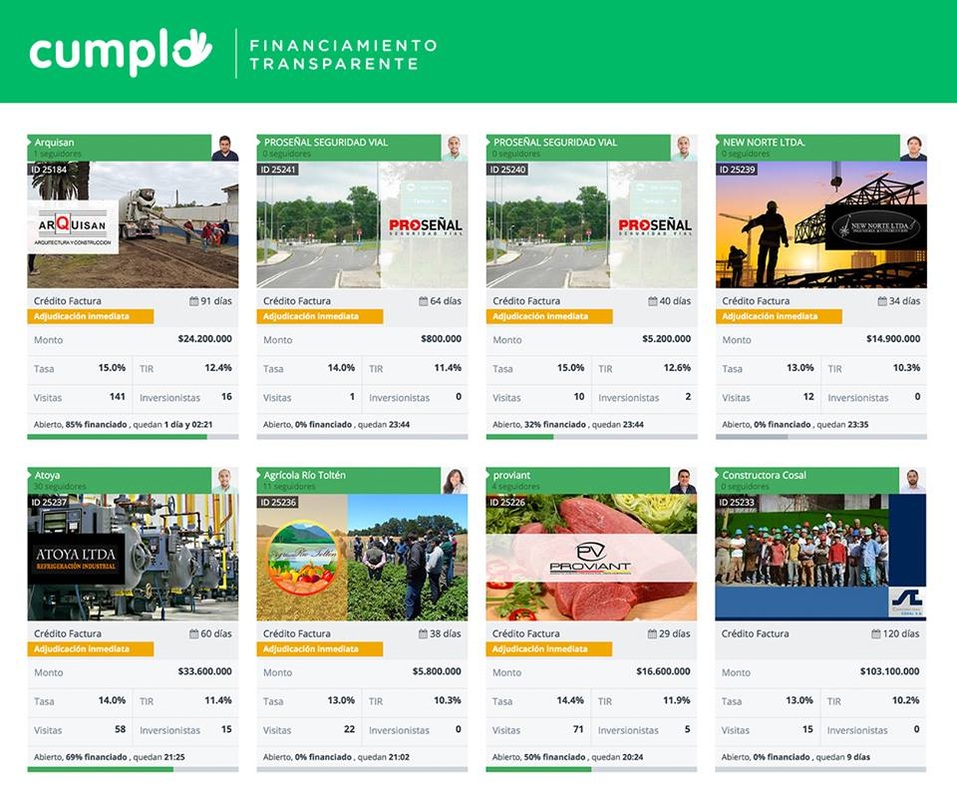

Cumplo is a cool Chilean startup founded four years ago, Cumplo created a unique on-line network that pools investors’ capital and loans it to small and middle Chilean companies, it works similar to a lending club. Cumplo connects investors (anyone with a Chilean bank account and tax number can invest in any opportunity) to pre-screened companies with a strong track record and solid fundamentals that are in search for cheaper capital to finance working capital or minor CapEx (Capital Expenditures).

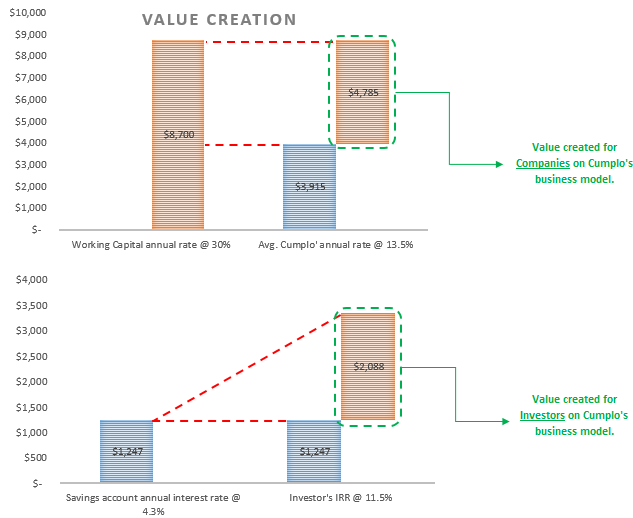

Cumplo started after a careful analysis of the Chilean banking system and low risk investment returns offered by the very same banks (savings account or T-bills) to investors, Cumplo’s founders noticed a huge spread and decided to pursue the idea of creating a safe/transparent alternative for solid small and middle businesses. According to Mr. Acuña, every opportunity brought to investors is subjected to a thorough financial assessment and risk analysis; this allows Cumplo to have a loan default rate of about 1%. Cumplo is one of those no brainer ideas that makes people wonder why nobody ever created, in my opinion, the business model is successful because it creates and capture value in a very simple and straightforward way. See figure below.

Cumplo started after a careful analysis of the Chilean banking system and low risk investment returns offered by the very same banks (savings account or T-bills) to investors, Cumplo’s founders noticed a huge spread and decided to pursue the idea of creating a safe/transparent alternative for solid small and middle businesses. According to Mr. Acuña, every opportunity brought to investors is subjected to a thorough financial assessment and risk analysis; this allows Cumplo to have a loan default rate of about 1%. Cumplo is one of those no brainer ideas that makes people wonder why nobody ever created, in my opinion, the business model is successful because it creates and capture value in a very simple and straightforward way. See figure below.

For this simple case study, company ABC borrows $29,000 thousands from a common working capital credit line at an annual 30% interest rate, if the same transaction is performed under Cumplo, company ABC saves $4,785. In the investor’s case, investing $29,000 with Cumplo returns $2,088 over the same amount invested at a Chilean’s savings account.

Although Cumplo is showing a strong growth for the last four years, there are clear challenges going forward. As a first mover, Cumplo has developed a new market that is now open for competition; companies with proprietary capital (high liquidity) can develop a similar platform and compete for strong small/middle businesses, which will pressure lending rates down. Cumplo’s current model is hard to scale and dependable on constant addition of new companies. As Cumplo disburse more loans, it will face greater default risk and necessity to create more corporate structure (i.e. robust compliance), this will change the business operational leverage by raising fixed costs.

Although Cumplo is showing a strong growth for the last four years, there are clear challenges going forward. As a first mover, Cumplo has developed a new market that is now open for competition; companies with proprietary capital (high liquidity) can develop a similar platform and compete for strong small/middle businesses, which will pressure lending rates down. Cumplo’s current model is hard to scale and dependable on constant addition of new companies. As Cumplo disburse more loans, it will face greater default risk and necessity to create more corporate structure (i.e. robust compliance), this will change the business operational leverage by raising fixed costs.